A Current Gift that Preserves Future Flexibility

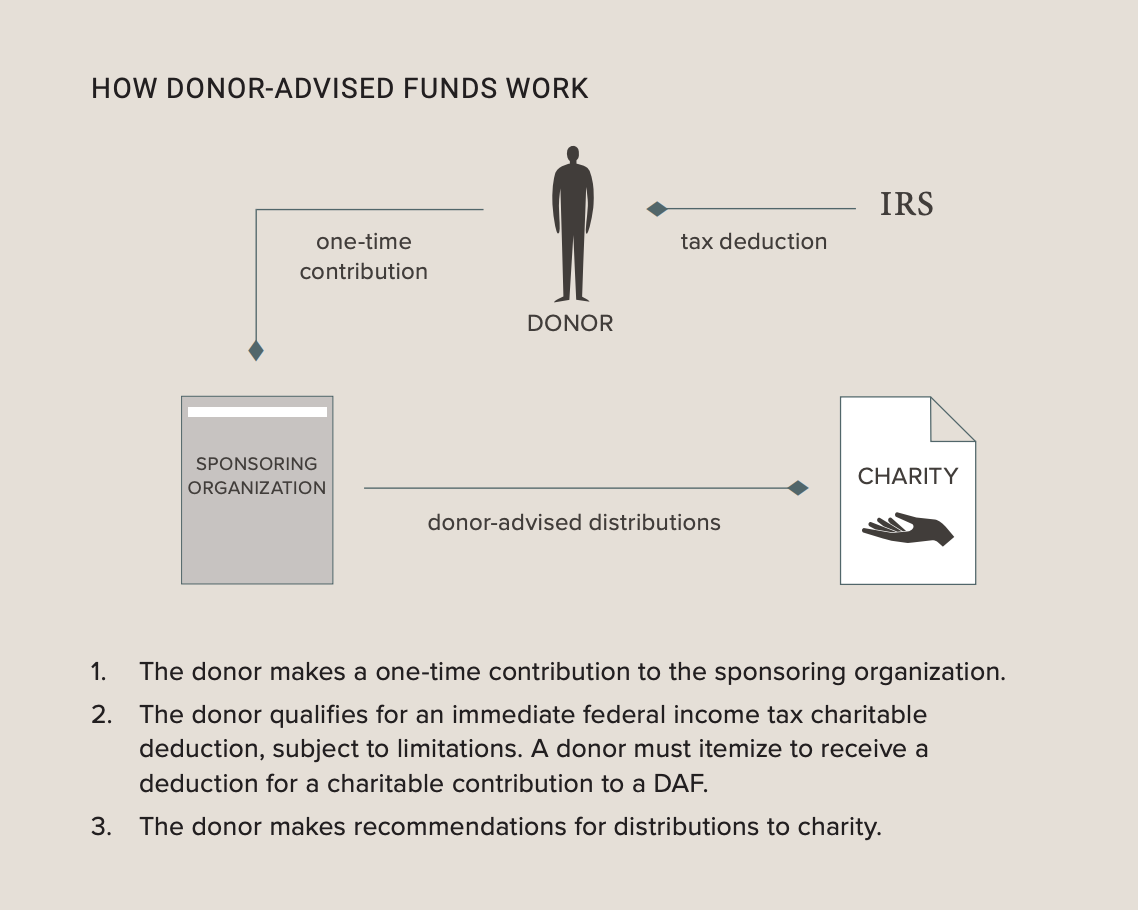

A donor-advised fund (DAF) is a contractual relationship between a donor and a sponsoring organization. The donor makes a charitable contribution to the sponsoring organization, which then owns the assets and administers the fund. The donor retains advisory privileges over the charitable donations that are distributed from the account. This arrangement qualifies the donor for an immediate income tax deduction for the amount of the contribution, even though funds won’t be distributed until later, when the donor suggests supporting a specific charity.

A donor-advised fund offers remarkable versatility in letting donors choose how they give at a time that works best for them. This unique “hands on” philanthropy is a personally satisfying giving option that also provides freedom from the administrative responsibilities of managing the account, including investment decisions.

As the following diagram shows, the initial contribution to a DAF is tax deductible for itemizers. Later, the donor can recommend distributions from the account (which are not tax deductible) under the terms of the DAF.

Donor-Advised Funds Offer Increased Appeal

Because of the high standard deduction, fewer taxpayers are itemizing their federal returns. To maximize the benefit of charitable deductions, some donors may choose to “bunch” donations—making larger, less frequent gifts—to exceed the standard deduction threshold. This strategy will also be useful starting in 2026 to help donors surpass the new 0.5%-of-AGI floor for deductions. A DAF can be an effective way to bunch gifts.

When you contribute to a donor-advised fund, your gift qualifies for a charitable deduction in the year of the gift. This means you can make a large, taxdeductible contribution to the DAF in one tax year and delay recommending distributions—or grants— from the account until later years.

NOTE: : Starting in 2026, nonitemizers will be able to deduct up to $1,000 (single filers) or $2,000 (joint filers) for gifts to public charities—excluding contributions to DAFs.

Advantages for Donors

There are many ways to make meaningful, personally satisfying gifts, so why would a donor-advised fund rise to the top of a donor’s list of ways to reach philanthropic goals? Here are some key DAF benefits to keep in mind.

Advisory privileges

Although the sponsoring organization owns and manages the DAF and is legally required to retain ultimate authority over distributions, advisory privileges are the key reason why donors select this gift option. DAFs can meet charitable planning goals in sensible and pragmatic ways.

EXAMPLE 1

Camila is a highly paid consultant who just signed a long-term creative services contract that included a substantial up-front bonus. She will be able to benefit from an itemized charitable tax deduction this year, so she makes a major contribution to a donor-advised fund. Her goal is to support her favorite charity on a long-term basis, specifically directing distributions to the work that, in her opinion, represents the greatest opportunity to make a meaningful impact. Camila is particularly pleased that she can use this charitable strategy that meets immediate needs while providing the flexibility to meet future charitable goals that are not yet specifically identified.*

EXAMPLE 2

Carter is about to receive a substantial inheritance from his father—part of it made up of retirement assets that will be taxable to him. Although he could opt to receive the retirement assets over time, he elects to receive them in full now. To offset the tax that will be due, he makes a tax-deductible contribution to a donor-advised fund. One of the motivating factors for Carter’s approach is the desire to honor his father’s memory by making an immediate grant from the DAF. He also appreciates the luxury of taking his time to consider how and when to make future grants. Carter benefits from a tax deduction now and looks forward to participating in meaningful philanthropy for years to come.

* Example for illustrative purposes only.

Timing and tax deductions matter

As the examples illustrate, eligibility for a charitable tax deduction can be an important part of planning. Although the primary motivation behind giving is the desire to make a philanthropic impact, it is wise to consider timing realities and how a gift can benefit the giver as well as the charitable organization. For instance, a particular year with a large or unexpected bump in taxable income can be an ideal time to consider a donor-advised fund because of the welcome tax deduction.

Timing can also be important for other reasons. For example, George and Sydney are nearing retirement and want to enjoy the benefits of a tax deduction while they are still working. They also want to segment their charitable funds from other funds set aside for planning purposes. With a DAF, they can make a substantial contribution during their working years, then make their grants to charity whenever the time is right for them.

An alternative to a private foundation

For many donors, a DAF provides a rewarding alternative to a private foundation. Like a private foundation, a DAF can offer satisfying, “handson” participation in deeply meaningful long-term philanthropic endeavors. Family members can work together to meet charitable goals and shape a family legacy. However, when compared to a private foundation, donors may find a DAF more appealing because it:

• is easier and substantially quicker to establish

• has no start-up costs

• enjoys substantially lower administrative fees each year

• can offer a greater tax deduction as a percentage of adjusted gross income (60% of AGI vs. 30% for a private foundation)

• is not subject to potential excise taxes

• is not subject to annual grant distribution requirements

• offers greater protection for donors who wish to make anonymous gifts

Even though the sponsoring organization has ultimate legal authority over grant distributions, many donors are more than content with the role of “advisor” in exchange for these benefits.

A Word from the IRS

When considering personal philanthropy, it is necessary to keep in mind the tax laws that apply to planned gifts. IRC §4966 describes three important requirements of a DAF:

1. Separate identification. The fund must be “separately identified by reference to contributions of a donor or donors.” This means the fund must be sequestered from the sponsor’s general fund and specifically identified by reference to a particular donor (or group of donors) in that all contributions must be attributable to the named donor (or group).

2. Ownership and control. The fund or account must be “owned and controlled by a sponsoring organization.” Under this section of the Code, “sponsoring organization” is defined as a public charity (not a private foundation) that has one or more donor-advised funds.

3. Advisory privileges. The “donor (or any person appointed or designated by such donor) has, or reasonably expects to have, advisory privileges with respect to the distribution or investment of amounts held in such fund or account by reason of the donor’s status as a donor.”

Planning Considerations

The following questions and answers may help you determine how a donoradvised fund might fit into your personal planning.

Are all sponsoring organizations the same?

No, they are not. Community foundations have been associated with donoradvised funds for several decades. More recently, many different types of charitable organizations have established sponsoring organizations to administer donor-advised funds. In addition, some financial companies have created sponsoring organizations. Each sponsoring organization can have unique rules regarding the donation required to begin the fund, how grants are made from the fund, and fees associated with the fund.

Are additional contributions allowed?

Generally, yes—however, as noted above, each sponsoring organization has its own rules.

Who can receive grants from a donor-advised fund?

Grants or distributions from a DAF must be made to qualified charitable organizations. The sponsoring organization may have requirements for grant amounts and frequency—remember that the sponsoring organization has ultimate legal authority over distributions from the DAF.

Can a donor pass a DAF on to others?

Some sponsoring organizations allow for the transfer of advisory privileges to another individual. Others allow you to designate a specific charitable organization to receive the funds in the account when you die.

A Simple, Rewarding Philanthropic Option

At their core, donor-advised funds are remarkably simple. They allow you to make a single donation that can benefit one or more charities through multiple grants from the DAF at different future dates, with minimal constraints on the timing of those grants. DAFs can be highly rewarding and useful for donors who want to make a charitable commitment now, benefit from a current tax deduction, and retain the right to “fine-tune” grant distributions or make multiple grants in the future.

Please contact us for more information about donor-advised funds and grants to our organization. It would be our pleasure to help you explore the possibilities associated with this flexible giving strategy

ABOUT THE COMMUNITY FOUNDATION OF BOONE COUNTY

The Community Foundation of Boone County exists to unite people, organizations, and philanthropy to create a thriving community for all. Since 1991, its leaders have worked to empower and engage local communities to make a difference right here in Boone County, while also leading a vision to collaboratively address the root causes of challenges facing Boone County in diverse and equitable ways. The Community Foundation continues to invest in the people working to fill local needs and has granted more than $31 million to nonprofit organizations and programs working to solve critical challenges in Boone County. With nearly $38 million in assets, the Community Foundation works with donors to create permanent funds for charitable giving, to strengthen Boone County for generations to come.