Long-Term Strategies

Smart personal planning means understanding how to achieve fi nancial, personal, and philanthropic goals. It means thinking about how to maintain a current lifestyle, keep up with investments, and take advantage of sound tax planning. It also means exploring creative gift plans that provide financial and tax benefits while helping you make satisfying gifts to charity.

While most tax planning takes place at year end, recent and continuing tax changes mean we need to expand our frame of reference beyond shortterm results. Let’s look at some longer-term strategies that can help you achieve personal planning objectives.

Personal Tax Deductions

Current income tax rules provide taxpayers with deductions for certain expenses, payments, and contributions when they itemize their tax returns. For some items, expenses must exceed a dollar threshold for the deduction to apply, so timing can be critical. Here are some basic ideas to be aware of when approaching income tax planning:

Interest: Some interest payments you make are deductible–for example, certain business expenses. If you are in a high-income year, you may want to seek professional advice on accelerating deductible interest payments prior to the end of your tax year.

Medical and dental expenses: Most out-of-pocket expenses for medical, dental, and vision care are deductible if they exceed certain thresholds of adjusted gross income (AGI).

State and local taxes: Several types of state and local taxes, combined with property taxes, are deductible up to a $10,000 limit.

Losses: Investment losses are deductible against investment gains. If you have incurred capital losses, it may be a good time to rebalance your portfolio. You can sell appreciated stock or other equities and off set the capital gains with your deductible losses.

Charitable contributions: Perhaps the most important deduction for many people is the deduction for charitable contributions. There are many ways to give to charity, and all are well worth exploring, as they can provide signifi cant tax savings and other fi nancial benefits.

Your tax advisor can answer questions about all these deduction rules.

Maximizing Tax Savings With A Gift of Stock

Prudent investing includes understanding how to balance risk and reward. When priorities change, so should investment strategies. If you plan to sell or trade stocks, it may be a good time to consider a gift of stock. Giving stock is an opportunity to align financial and charitable goals in a taxeffi cient way.

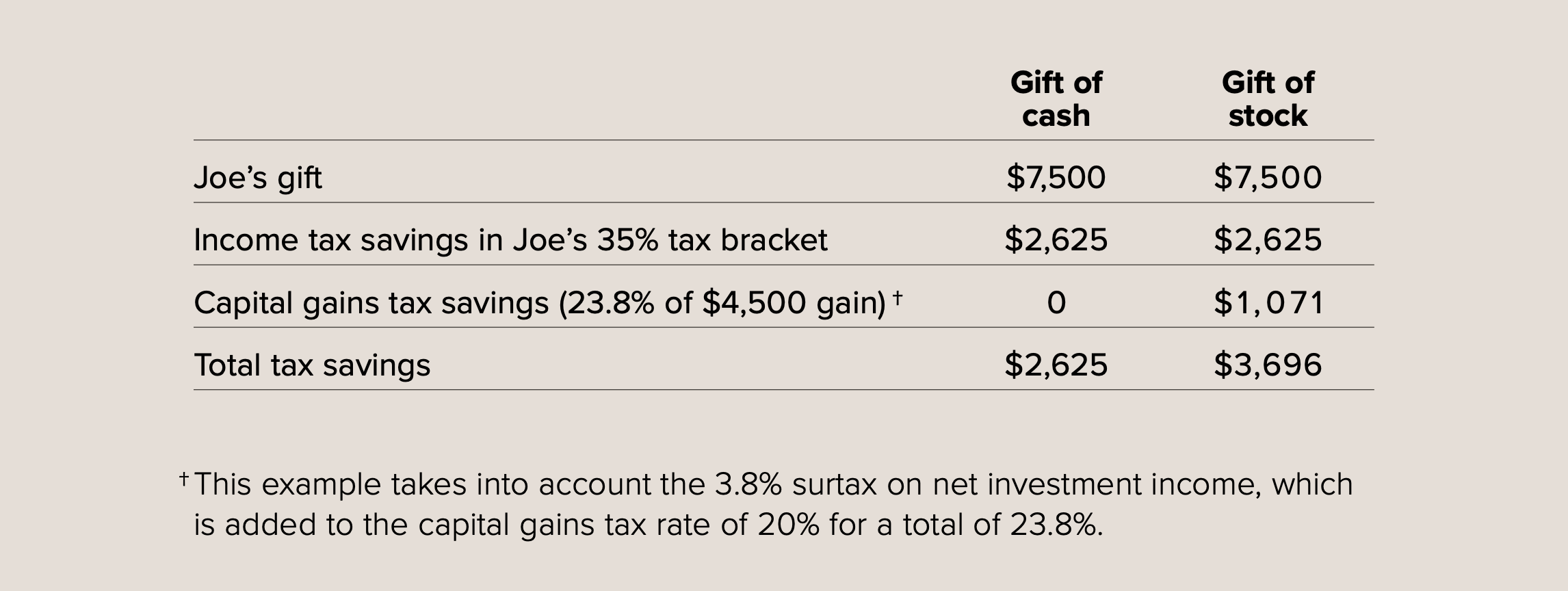

There is a double tax advantage to giving an outright gift of appreciated stock. First, if you itemize, you can take a regular income tax deduction equal to the stock’s fair market value for a gift of stock you held for more than one year. Second, you owe no capital gains tax on the transfer.

EXAMPLE: Joe usually gives us a check for $7,500 at year end. This year, he thinks about the double tax advantage of giving appreciated stock. He purchased 100 shares of stock years ago for $3,000. Those shares are now valued at $7,500. Because he itemizes his return, he can enjoy a double tax benefit if he gives the stock to us.*

* Example for illustrative purposes only.

Congress included this double tax advantage in the income tax laws to encourage gifts of appreciated stock. Yet, surprisingly, many investors remain unaware of this benefi t and fail to take advantage of this opportunity.

Funding Life Income Plans With Stock: Tax Savings Plus an Income Stream

A gift of stock can be used to fund a life income plan, such as a charitable remainder trust or a charitable gift annuity.

CHARITABLE REMAINDER TRUST

A charitable remainder trust provides an income stream to one or more benefi ciaries for a set number of years or for life, then distributes the remainder to a charitable organization. The present value of that future remainder expected to go to charity provides an income tax deduction for the person who creates the trust. Let’s look at an example featuring a charitable remainder annuity trust (CRAT).

Joy (age 78) purchased 400 shares of stock 20 years ago for $75,000. Today, the stock is worth $450,000. Joy is receiving $9,000 a year in dividends, but she would like more income. After discussing matters with her advisors, Joy decides to use the stock to fund a charitable remainder annuity trust and she names us as the beneficiary.

Joy transfers the appreciated stock to a charitable remainder annuity trust that will pay her $22,500 (5%) a year and also give rise to an income tax charitable deduction of $278,978 (based on an AFR of 4.4%). Joy’s charitable deduction will result in tax savings of about $103,222 in her 37% tax bracket if she itemizes. Plus, Joy can reduce the $89,250 capital gains tax that she would have owed ($375,000 gain x 23.8%) had she sold the stock. We will receive the principal of the trust at her death. Joy appreciates the substantial financial and tax benefi ts and is delighted to know that her gift will have an impact on our work.

CHARITABLE GIFT ANNUITY

A charitable gift annuity is a simpler arrangement that follows the same principle and can also be funded with appreciated stock. A gift annuity is a split gift—part charitable gift and part annuity purchase. When you fund a gift annuity, we agree to pay a percentage of the gift amount on a regular basis to one or two benefi ciaries for life. The gift portion creates an immediate income tax deduction for you and the annuity portion provides a lifetime income based on the age of the annuitant(s) and the total amount donated to charity. (You can choose to name any person as the annuitant).

Real Estate

There are many diff erent ways to make a gift of real estate.

- Outright gift—directly transfer the title to us, qualify for a substantial income tax deduction, and owe no capital gains tax on any appreciation.

- Bargain sale—sell your home to us for less than its fair market value and qualify for a deduction for the gift portion (the diff erence between the selling price and the fair market value).

- Gift of a remainder interest—give your house to us, but retain the right to live in it as long as you want—even for life—while qualifying for an immediate income tax deduction for the present value of our remainder interest (the appraised value of the house minus your life estate in the property).

- Life income gift—transfer the real estate into a charitable remainder trust or a charitable gift annuity to make a gift and create an income stream.

Social Security

Social Security was originally designed to provide a safety net to keep older Americans from falling into poverty, and many retirees continue to depend on it. However, affluent retirees are able to save that money and use it to help their children or give all or part of this income to charity.

There are many ways to include Social Security income in your retirement and charitable planning.

- Make an outright gift of your Social Security payment to our organization and claim an itemized income tax deduction.

- Purchase a charitable gift annuity at the end of the year with your collected monthly Social Security payments. Buying gift annuities every year is a strategy known as laddering—as you grow older, you will likely earn a greater payout rate for each successive annuity.

- Contribute to a charitable remainder unitrust (CRUT) at the end of the year with your collected monthly Social Security payments. A CRUT is an irrevocable trust that pays a percentage of the value of the trust assets (as revalued each year) to a lifetime benefi ciary—either you or someone you name. At the conclusion of the trust, remaining assets are distributed to a charitable organization. After you create the CRUT, you can make additional contributions that increase the value of the trust, and you qualify for an income tax deduction for the present value of the expected remainder from each contribution.

- Contribute to an existing endowment using your Social Security payments. This is a creative way to multiply the impact of your gift, since an endowment spends only a percentage of the total value (or the interest from its funds) so that your gift continues to support your favorite programs year after year.

With careful planning, Social Security income can support our mission and provide you with valuable tax benefits.

The Next Step

Each family and every situation is diff erent. We invite you to contact us with your questions or concerns or for a more detailed discussion of the various strategies we’ve outlined here. It would be our privilege to help you explore the role philanthropy can play in meeting your overall planning, retirement, or year-end goals.

ABOUT THE COMMUNITY FOUNDATION OF BOONE COUNTY

The Community Foundation of Boone County exists to unite people, organizations, and philanthropy to create a thriving community for all. Since 1991, its leaders have worked to empower and engage local communities to make a difference right here in Boone County, while also leading a vision to collaboratively address the root causes of challenges facing Boone County in diverse and equitable ways. The Community Foundation continues to invest in the people working to fill local needs and has granted more than $31 million to nonprofit organizations and programs working to solve critical challenges in Boone County. With nearly $38 million in assets, the Community Foundation works with donors to create permanent funds for charitable giving, to strengthen Boone County for generations to come.